Programme Start Date: 29th March, 2024

Programme Start Date: 29th March, 2024

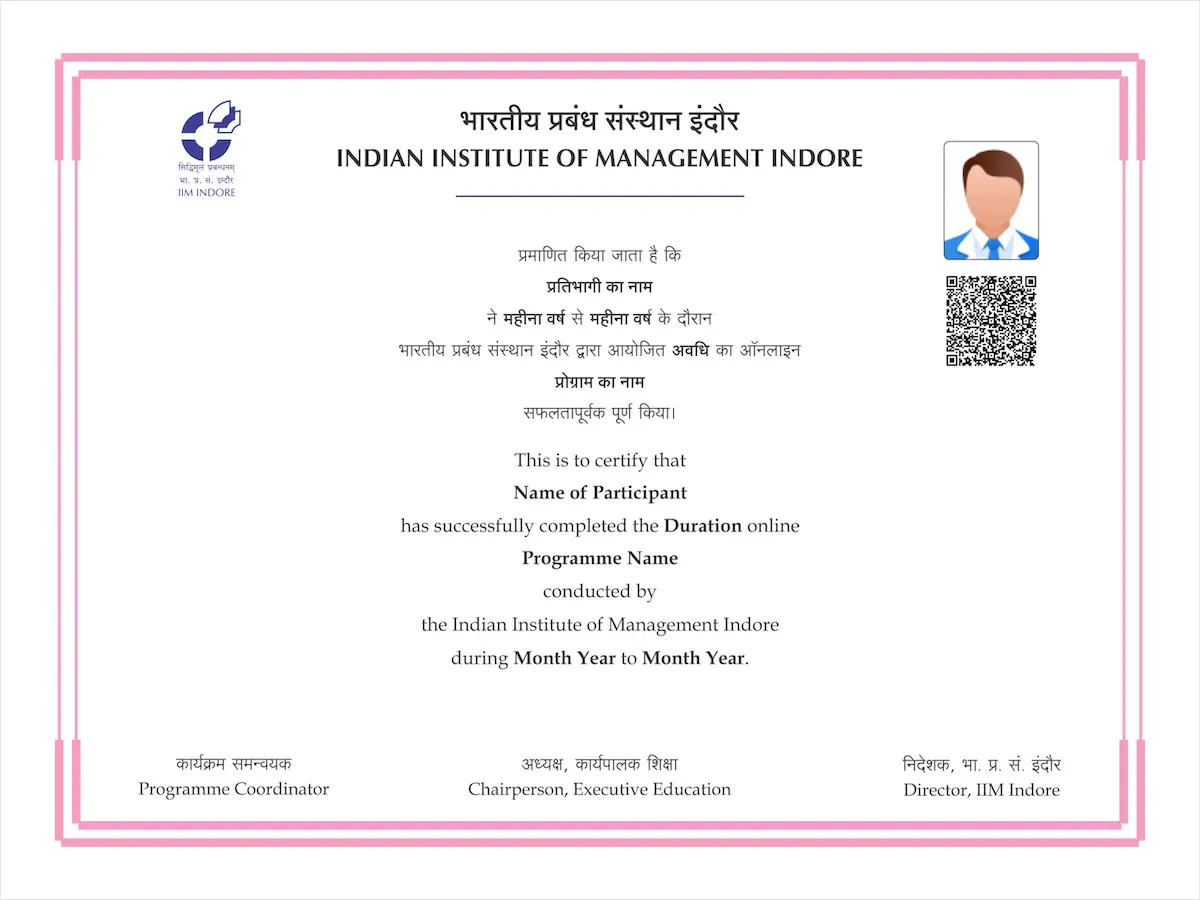

Certificate from IIM Indore

Certificate from IIM Indore

Direct-to-device

Direct-to-device

Content

Check the course module of the IIM Indore applied financial risk management programme.

- Understanding the Contours of Uncertainty, Risk, and Complexity

- Approaches Towards Risk Management: Theory and Practice

- Risk Management Framework for Financial Institutes: The Philosophy and Contours of Basel Framework and Beyond

- Enterprise Risk Management: A Holistic Risk Management Framework for Non-financial Firms

- Complexity Science and the Emergence of a New Paradigm of Risk Management

- Sample and Population Statistics

- Statistical Inference and Hypothesis Testing

- Measure of Dependence (Correlations)

- Linear Single and Multiple Regressions

- Time Series Analysis and Forecasting

- Application of Quantitative Analysis using R and Python

- Application of Machine Learning for Risk Management

- Structure and Functions of Financial Institutions

- Financial Statement Analysis and Bank Valuation

- Understanding Risk in the Financial Institutions

- Risk in the Equity and Bond Markets

- Futures and Hedging Strategies

- Options and Hedging Strategies

- Interest Rate Futures and Hedging Strategies

- Options Greek

- Valuing a Fixed Income Security: The Relationship Between the Interest Rate and the Price of a Debt Asset

- Understanding and Predicting the Yield Curve

- The Fixed Income Portfolio Strategies and the Interest Rate: Sources of Interest Rate Risk Affecting the Fixed Income Portfolio

- Duration, Convexity, and Single Factor Risk Management

- Immunisation and Other Passive Portfolio Management Strategies

- Using Market-based Risk Hedging: Interest Rate Futures and Interest Rate Swaps

- Introduction to Simulation in Financial Decisions

- Analysing NPV Under Uncertainty

- Cash Balance Analysis and Investment Modelling

- Revenue Management Using Simulation

- Short- and Long-run Relationship and Their Assessment

- Assessment of Volatility Model

- Analysis of Value-at-Risk and Expected Shortfall

- Portfolio Management

- The Nature of Credit Risk: The Challenges and Peculiarity of Managing Credit Risk

- Credit Default Swap

- Asset-backed Securities

- Structural Models for Credit Risk (Merton, KMV)

- LGD Estimations: LGD Model and its Applications

- Exposure of Default-EADF Modelling

- Liquidity Risk, Principles, and Metrics

- Liquidity Adjusted Value-at-Risk Under Normal and Stressed Market

- Cash Flow Modelling, Liquidity Stress Testing